- Example active heading

- Example heading

Executive summary

The Lendio SMB Lending Index is a measure of how accessible capital is to Small Business borrowers. Lendio analyzes the business profiles of over 14,000 business owners who receive funding offers through our marketplace quarterly, and compares average credit score,* monthly revenue, and time in business of every company that received a financing offer against a framework informed by historical averages.

Every quarter, in parallel to this analysis, we survey both SMB lenders and borrowers to better understand the dynamics influencing accessibility to capital for Small Businesses, and provide insight into what lenders are anticipating the market will see in the following quarter. Previously published as two reports, the SMB Lending Index, and the State of Small Business Lending, these insights have been combined to create a comprehensive view of the state of small business lending.

Key Insights

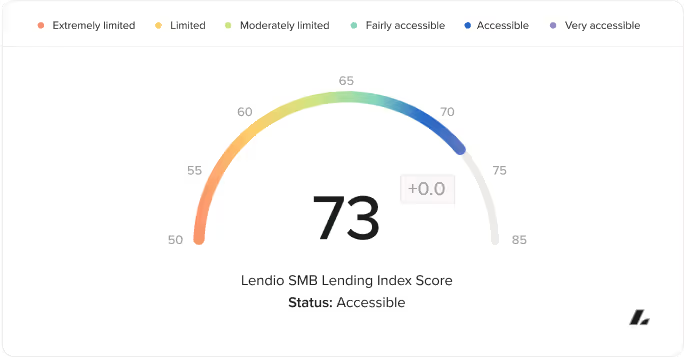

- Lendio is seeing credit criteria holding steady, with credit requirements for small businesses to qualify for a loan comparable in Q1 2025 compared to Q4 2024. This is reflected in Lendio’s SMB Lending Index score, which moved no points from Q4 2024, and up 9 points from Q3 2024.

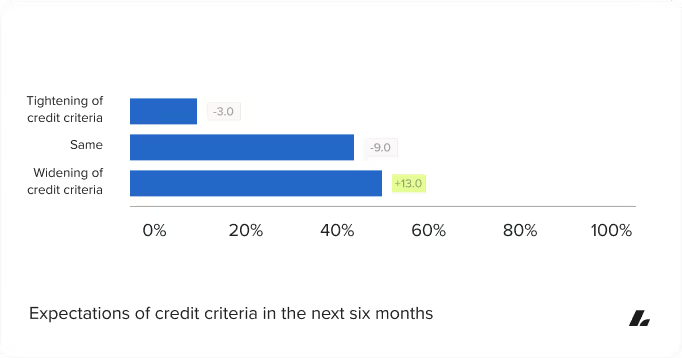

- 50% of lenders expect credit criteria to loosen further over the next quarter, while 41% expect qualification requirements to stay about the same. Few lenders felt that criteria for small business financing would tighten over the next quarter.

- 59% of lenders have a positive perception of an SMBs’ ability to access capital in the current market, stating that SMBS have positive (above market average) or very positive (Majority of SMBs can access the capital they need) access to capital.

- While the majority of lenders have a positive perception of SMBs’ access to capital, less than half (32%) of small business owners were “very satisfied” or “satisfied” with amounts and terms they were offered. 26% of SMBs indicated a neutral level of satisfaction, while 21% were “unsatisfied” or “very unsatisfied” with amounts and terms offered, and 22.7% of SMBS who applied for funding reported receiving no financing offer at all.

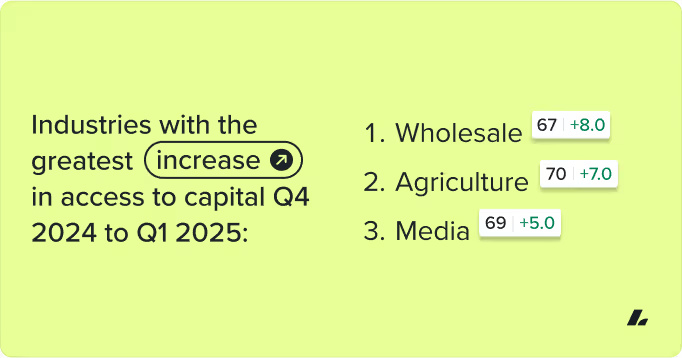

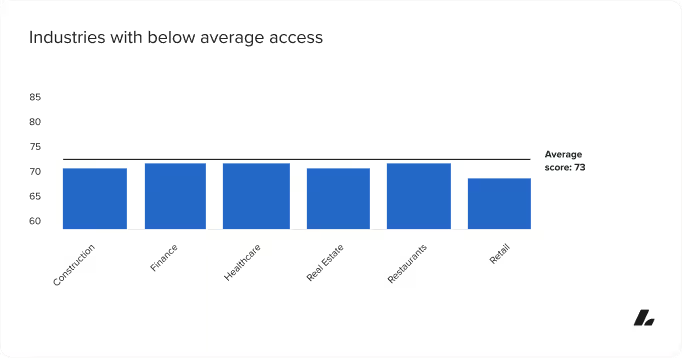

- The wholesale, agriculture and forestry, and information and media industries saw increased access to capital from Q4 2024 to Q1 2025. Retail, construction and finance saw a decline in access to capital during this period.

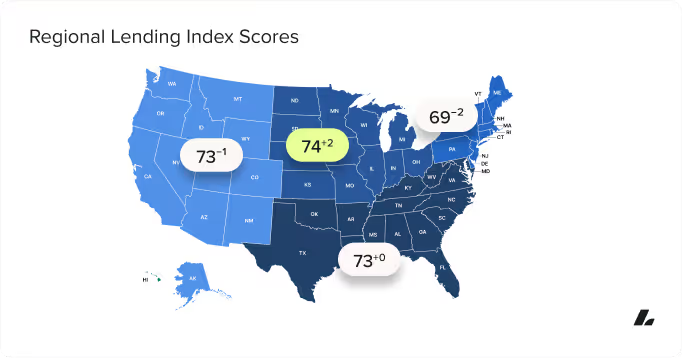

- Small businesses in Massachusetts had the most access to capital in Q1 2025, scoring 6 points above the national average. Hawaii fell 11 points below the national average from Q4 2024, indicating that small businesses in this state experienced tightening credit criteria.

Lendio SMB Lending Index Score: 73(+0)

Q1 2025

Q4 2024 Score: 73

Lendio is seeing credit criteria holding steady, with credit requirements for small businesses to qualify for a loan in Q1 2025 comparable to those in Q4 2024. Credit criteria loosened noticeably, from 63 in Q3 2024 to 73 in Q4 2024, and Q1 2025 respectively. Based on the feedback we gathered from lenders, we anticipate this loosening of criteria will continue through 2025.

What does the Lending Index Score mean?

Lendio’s SMB Lending Index measures how accessible business financing is to small business owners, with a higher score indicating greater accessibility. The score is based on the business profile of the 14,000+ small businesses offered financing in Lendio’s marketplace in a quarter. The report’s methodology section provides a full breakdown of how the score is calculated.

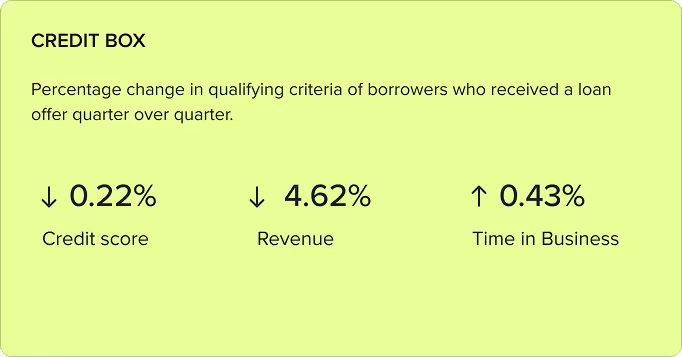

Credit box

Lendio measures changes to borrowers' qualifying credit score, monthly revenue, and time in business over a quarter period.

Lender sentiment

Most lenders are bullish on financing opportunities for small businesses in the next quarter. 50% of lenders expect their credit box to widen, easing credit qualifications for loans. 18% of surveyed lenders specifically mentioned positive economic signals, easing regulatory burdens, and/or the incoming administration as factors in their answers. "The election and the perceptions of the lessening of regulatory burdens are fostering an environment where more business owners are considering growth over the next six months,” said Tim Mages of Expansion Capital Group. “However, uncertainty surrounding tariffs and government cuts in early February from the new administration has led to cautious decision-making. As business owners work to assess the potential impact of tariffs on their cost structure and sales demand, the overall demand for capital has been mixed.”

41% of lenders see current criteria remaining the same in the coming quarter, but many see opportunities to optimize their processes and products with enhancements to serve more customers beyond credit requirements. “We see our credit box both tightening and widening,” said Jason Solomon of Fora Financial. “We will be taking on significantly more risk in areas we feel are worth it, and tightening populations where we have seen unrelenting write-offs.”

Other lenders who indicated their credit criteria would remain the same next quarter cited adding new products, improving approval terms with changes to pricing, terms and dollar amount, and speeding up qualification processes with innovation - including generative modeling - to serve a wider variety of SMBs.

Only 9% of lenders foresaw any tightening of credit criteria in Q2.

“The election and perceptions of the lessening of regulatory burdens is creating an environment where more business owners are looking at growth than 6 months.”

In January 2025, Lendio surveyed 22 small business lenders about their perceptions of the current small business lending market and their optimism for the future.

What is your perception of an SMB's ability to access capital in the current market?

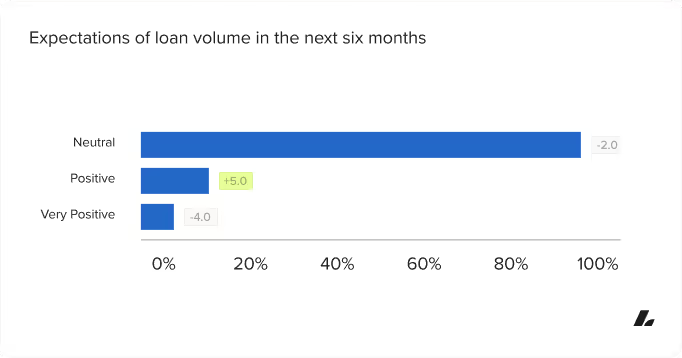

Expectations of loan volume in the next six months

Expectations of credit criteria in the next six months

SMB sentiment

Lendio surveyed 1,400 small business owners to better understand the role financing plays in the success of their business, their experience with the current lending environment, and their expectations for the future.

Industry analysis

Three industries saw tightening qualification criteria quarter over quarter.

Three industries saw loosening qualification criteria quarter over quarter.

Compared to Q4 2024, the retail, construction and finance industries experienced tightening credit standards, leading to decreased access to capital. All three industries have moved below the national average of access to financing.

Wholesale, agriculture and forestry, information and media, real estate and transportation experienced the greatest relaxation of credit standards, leading to increased access to capital. However, access to capital for real estate industries is currently below the national average.

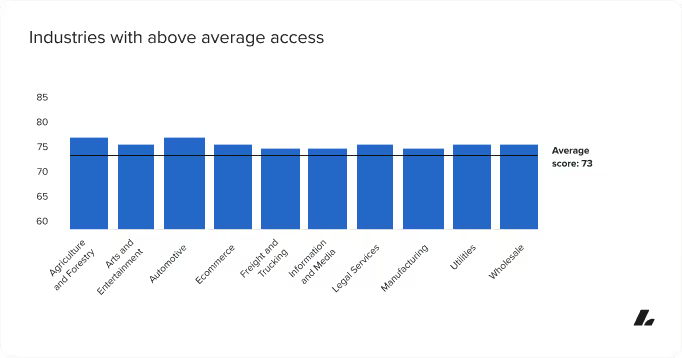

Industry scores are calculated by taking the average credit score, time in business, and monthly sales of every business in that industry offered financing through Lendio’s marketplace in a given quarter. Higher scores indicate a lowering of requirements to qualify for funding, increasing access to capital. Lower scores indicate a tightening of requirements to qualify for financing, decreasing access to capital.

Regional analysis

Lendio conducted a regional analysis of the data to uncover trends in the Northeast, Midwestern, Southern, and Western regions, according to Census regional divisions of the United States.

Northeast:69 | -2

The Northeast region saw a decline in access to financing Q1 2025, with only one state at or above the national average. Massachusetts rose above its previous Q4 2024 score by 6 points, leading Northeastern states in access to financing. Vermont increased 4 points above its previous Q4 2024 score, but still sits well below the national average.

Midwest:74 | +2

The Midwest region led the nation in more access to financing, with more than half of states performing at or higher than the national average.

Ohio and South Dakota saw a nine-point increase in lending sentiment score from Q4 2024.

South:73 | +0

Southern states performed second best against other regions. The Southern region saw no change in sentiment score from Q4 2024, and most states come in at or slightly above the national average for business financing access. However, Georgia, Kentucky, Maryland, North Carolina and South Carolina lead the Southern region with better than average access to financing.

West: 70 | -1

Western states saw a decline in business financing accessibility, slipping one point from Q4 2024. Most states fell below average, with only Arizona, New Mexico, Nevada and Washington exceeding the national average.

SMBs' need for access to financing is critical.

75% of small businesses reported that they consider access to financing very important for the survival of their business. 66% of small businesses describe access to financing as the most important factor for business growth.

Additionally, 49% of small business owners said if they consistently had access to financing their business needs, they would see a transformational increase in revenue, while another 43% said consistent access to financing would create a significant increase in revenue.

In spite of the illustrated importance of SMB lending, 23% of small business owners who applied for financing didn’t receive any offers.

“Access to capital is the heartbeat of our communities. Small business owners have been forced to rely on personal savings and outdated lending practices that hold back their potential. When we reimagine financing to be as nimble, human, and tailored as the entrepreneurs we serve, we’re not only fueling individual dreams – we’re driving innovation and sustainable growth across our economy. It’s time to put small businesses at the forefront and give them the funding that sparks their success.”

The current state of the lending market for SMBs.

The outlook from lenders is optimistic for SMBs access to financing. 59% of lenders we interviewed had a positive, or very positive perception of an SMB’s ability to access capital in the current market, and 86% of lenders saw the quantity of SMB loans they issue in the next quarter growing. 10% of lenders saw the number of loans issued staying the same. Only 5% of lenders saw the number of loans they issue in the next quarter shrinking.

“Barring something unpredictable, with a new administration taking over, the economy’s health will be at the forefront, and we believe companies will invest into their businesses.”

Jason Solomon, Fora Financial

Jason Solomon, Fora Financial

Although most lenders are feeling positive about SMBs' access to capital in the current market, with several foreseeing a loosening of the credit criteria necessary to secure a loan, SMBs are feeling lukewarm about the financing options they’ve been offered. Less than half (32%) of small business owners surveyed indicated they were “very satisfied” or “satisfied” with the amounts and terms they were offered. 26% of SMB owners indicated a neutral level of satisfaction, with the financing options not fully meeting their expectations for amounts, but were acceptable.

21% of SMBs indicated they were “unsatisfied” or “very unsatisfied” with the amounts and terms they were offered.

According to Lendio data, the median amount offered to a small business is typically 55% of what they were looking for, with an average term length of 16 months.

Lenders also note a qualification gap in the SMB lending market. “The higher end of the SMB spectrum has been quite robust. The other side of this discussion is that there are a lot of SMBs - based on files we review - that are over-levered or credit challenged. Thus, while options are available, the lower end of the market appears to have tightened due to performance challenges,” said Tim Mages of Expansion Capital Group.

A clear preference for loan product type.

According to our survey, SMBs have a clear preference for business financing by financial product type. The top three most preferred types of business financing among SMBs are business lines of credit, SBA 7(a) loans, and business term loans. On the other hand, there are some types of financing that fewer SMBs seek out. These include factoring, commercial real estate loans, and revenue-based financing.

SMBs' most commonly preferred type of business financing:

- Business line of credit (45%)

- SBA 7(a) loan (43%)

- Business term loan (34%)

SMBs' least commonly preferred type of business financing:

- Factoring (3%)

- Commercial real estate loan (7%)

- Revenue-based financing (13%)

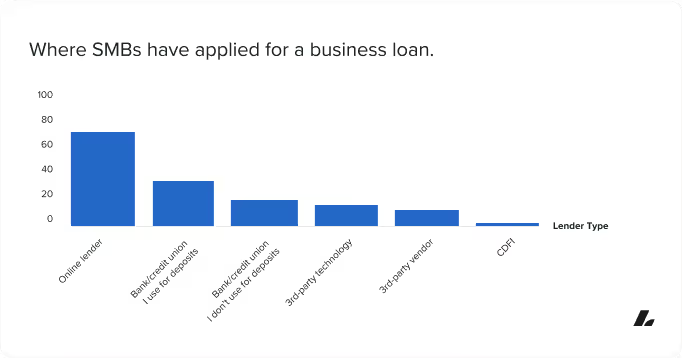

These preferences are largely mirrored in the financing SMBs report receiving.

Most commonly received form of business financing:

- Business term loan (26%)

- Business line of credit (24%)

- Revenue-based financing (24%)

Least commonly received form of business financing:

- Factoring (4%)

- Commercial real estate loan (7%)

- Equipment financing/ leasing (18%)

SMBs are pushing for a fully digital loan experience.

SMB owners are expressing strong preference for online experiences when pursuing a loan. 62% of respondents indicated they would prefer some or all of the loan application process to be online, while only 2% of SMB owners said they preferred to get a loan entirely in person.

SMB owners also have expectations about the length of the process. We asked respondents how long they expect each step of the application process to take.

Most SMBs expect each stage of the financing process to take one business day or less. These small business owners have more patience to wait to receive funds from the lender, or bank. 40% expect funds within 1 business day (40%), or 2-3 business days (31%).

73% of small business owners report that the loan application process took less than a week from researching lenders to receiving a final decision.

SMB owners who applied for a loan were asked about their satisfaction with the time each stage of the loan application process took.

The highest levels of satisfaction (“satisfied” or “very satisfied”) were found in completing the loan application (60%), and in receiving funds from the loan (44%).

Timing of the loan approval decision stage had the highest dissatisfaction (12%), with more SMB owners reporting they were “dissatisfied or very dissatisfied” at this stage. The loan approval decision stage also had the highest level of neutral opinion (26%).

.avif)

Earning small business loyalty.

67% of small business owners have no preference for where they get a loan from, leaving banks and financial institutions potentially exposed to competitors courting their depositors with loan offerings.

“Banks have continued to tighten credit criteria especially with the inflationary concerns, leaving more of a void that fintechs are attempting to solve.”

Speed of the loan application process plays a factor for small business owners who apply with the bank or credit union they deposit with as well. 26% said they are not willing to spend more than 60 minutes on a small business loan application at their bank before they’d consider applying elsewhere, while 24% are not willing to spend more than 30 minutes before considering another financing institution.

Lending options are critical to retaining SMB depositors.

Most small business owners haven’t considered moving their deposits to another bank (69%), but 31% have. The reasons for those who considered a move were: unmet business lending needs (39%), a better online or mobile banking experience (36%), poor customer service (27%), more convenient branch or ATM locations (25%) and unmet personal lending needs (8%).

.avif)

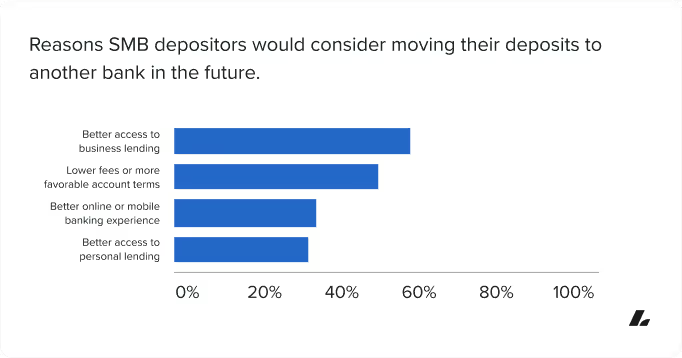

But financial institutions shouldn’t celebrate the majority of loyal small business owners yet. We asked small business owners who haven’t thought about moving their deposits to another bank, “what would make you consider moving your deposits to another bank in the future?”

56% said better access to business lending would make them consider a switch to another bank. Other top reasons for considering a move were lower fees or more favorable account terms (46%), a better online or mobile banking experience (32%), or better access to personal lending (30%).

“Credit access has emerged as the pivotal factor in maintaining SMB depositor loyalty,” said Philip Taliaferro, Chief Growth Officer at Lendio. “The recent rate run-up and the Silicon Valley Bank collapse have driven a dual shift: business owners are sharpening their focus on savings yield, and banks are increasingly demanding that new lending relationships also translate into deposit commitments. Leading institutions are now leveraging sophisticated analytics to identify and support at-risk deposit relationships. By integrating deposit primacy with lending, banks will not simply react to market pressures, but strategically position themselves for sustainable growth in a rapidly evolving financial landscape.”

Banks can do more to raise awareness with SMB depositors.

50% of small business owners say they don’t know if the bank they use for deposits has the right loan options for them.

Our survey asked if small business owners recalled seeing advertisements for small business loans from their primary bank, and if so, how frequently. 43% reported they didn’t recall seeing any advertisements from their primary bank in the past 6 months, while some saw them only a few times in the past few months (19%) or once or twice a month (23%). Only 15% saw advertisements for small business loans from their bank very frequently (16%).

When asked what type of small business loan advertisement from any lender would most encourage SMBs to apply for a loan, the responses were fairly even, lead by pre-approval offers, competitive interest rates, and speed to approval and funding.

Banks facing challenges with SMB awareness of financing options and products are not alone. Noting why his perception of an SMBs' ability to access capital in the current market is neutral, Ryan McMahon of Quantum Lending solutions said, "There's a lack of knowledge about alternative lending for non-bankable customers, and there are new businesses starting up all the time."

Methodology

SMB Lending Index

To calculate the score, Lendio pulls the average credit score,* monthly revenue, and time in business of every company that received a financing offer through our marketplace in the given time frame of Jan 1, 2025 - March 12, 2025.

These averages are then compared against a framework developed by historical averages at times of lower and higher credit requirements. The framework is also adjusted based on changes in the overall borrower mix. The top 95th percentile was removed from time in business, and average monthly revenue, to eliminate outliers relative to the population being measured in industry and region. Average monthly revenue is adjusted for inflation using data from the Bureau of Labor Statistics. The final score is the average of the three scores calculated for credit score, monthly revenue, and time in business. Calculations for this quarter’s report were based on a regional analysis of 14,147 distinct borrowers, and an industry analysis of 14,271 distinct borrowers.

Survey

In January 2025, Lendio surveyed 22 lenders, including banks and online lenders, and 1,432 small business owners, to gauge their sentiment towards the current small business lending market.

*Credit score averages are based on businesses’ selfreported credit scores from the respective populations of 14,147 borrowers by region, and 14,271 borrowers by industry.

FAQs

The information provided on this blog is for general informational purposes only, and should not be construed as business, legal, tax, accounting or financial advice. Readers should consult with a qualified professional before making any business, financial, or legal decisions. The views and opinions expressed in this blog are solely those of the authors and do not necessarily reflect the official policy, position, or endorsements of Lendio. While Lendio strives to keep its content current, it is accurate only as of the date posted. Business trends, financial conditions, regulations, and offers are subject to change without notice and may no longer be relevant or available. Lendio expressly disclaims all liability for any reliance placed on this information. By accessing this blog, you acknowledge and agree that Lendio shall not be held liable for any direct, indirect, incidental, consequential, or other damages arising from your use or reliance on the information provided.

Quickly compare loan offers from multiple lenders.

Applying is free and won’t impact your credit1.